Health Insurance FAQ

Sometimes insurance terminology can be confusing. Here are a few that may help you when purchasing affordable health insurance.

Deductible

A deductible is a specific dollar amount your health insurance plan may require you to pay out of pocket toward covered medical care each year, before your health plan begins to pay for covered medical expenses.

Your annual deductible can vary significantly from one health insurance plan to another. THe higher the deductible the lower your monthly payment

Coinsurance

Coinsurance refers to the amount that you are required to pay for a medical claim, apart from any copayments or deductible that may also be applicable. For example, if your health insurance plan has a 20% coinsurance requirement (and does not have any additional copayment or deductible requirements), then a $100 medical claim would cost you $20, and the insurance company would pay the remaining $80. Coinsurance, deductibles, and copays constitute out-of-pocket costs for health insurance.

In an example of 80/20, 80 is paid by the insurance company and 20 by the insured.

Copayment or Copay

A copayment (or “copay”) is a monetary charge that your health insurance plan may require you to pay in order to receive a specific medical service or supply. For example, your health insurance plan may require a $50 copayment for an office visit or brand-name prescription drug.

Maximum Out of Pocket

A limitation on all cost-sharing for which patients are responsible under a health insurance plan. Once you have reached tis the insurance company then pays 100%. This out-of-pocket limit (or out-of-pocket maximum) does not apply to premiums, balance-billed charges from out-of-network health-care providers, or services that are not covered by the plan.

Health Insurance FAQ

Premium

Copay

Deductible

Coinsurance

Out-of-pocket maximum

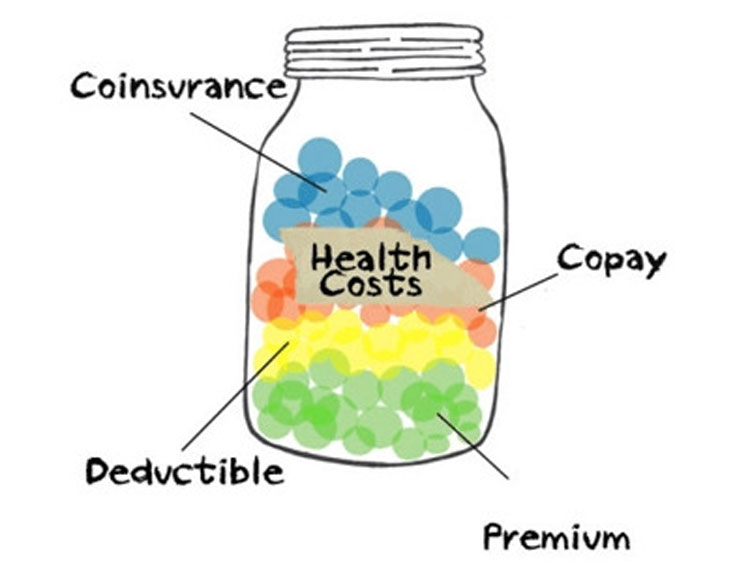

How they all work together

Health insurance policies can have a variety of cost-sharing options. Some policies have low premiums and high deductibles and out-of-pocket maximum limits, while others have high monthly rates and lower deductibles and out-of-pocket limits.

In general, it works like this: You pay a monthly premium just to have health insurance. When you go to the doctor or the hospital, you pay either full cost for the services, or copays as outlined in your policy. Once the total amount you pay for services, not including copays, adds up to your deductible amount in a year, your insurer starts paying a larger chunk of your medical bills, typically 60% to 90%. The remaining percentage that you pay is called coinsurance.

You’ll continue to pay copays or coinsurance until you’ve reached the out-of-pocket maximum for your policy. At that time, your insurer will start paying 100% of your medical bills until the policy year ends or you switch insurance plans, whichever is first.

Dental Insurance FAQ

How does dental insurance work? What do I pay for?

Premium

Deductible

Coinsurance

Copay

Can I buy dental insurance without having health insurance?

What do most dental insurance plans cover?

Is there a waiting period for dental insurance once I’m covered?

What is the difference between in-network and out-of-network care?

Cost. In-network dentists agree to accept a lower negotiated rate on services, meaning you pay less before your insurance carrier even gets involved. Non-network dentists can bill a patient for any remaining amount up to the billed charge.

Finally, when you stay in-network, you usually do not have to submit claims yourself. The dental office will handle the paperwork, saving you the cost of your time.

It’s a good idea to check on the number of dentists near you who are in-network before you buy a dental plan. If you already have a dentist, be sure to confirm if he or she is in-network. By choosing an in-network provider, you are making dental care more affordable for yourself.

Life Insurance FAQ

How can I determine whether I need life insurance?

What kind of things does life insurance cover?

What is a beneficiary?

The beneficiary is the person or entity named as the recipient of your policy’s death benefit. It can be a family member, a person unrelated to you, or even a business or other organization. You choose the beneficiary on your own — you don’t need permission from the insurer or the beneficiary. You can also choose more than one beneficiary and designate how you want the death benefit to be split among them, and name contingent beneficiaries in case the primary beneficiaries predecease you.

Your insurer will automatically disburse the death benefit if you die, but it’s still a good idea to tell any beneficiary about the policy so they will be prepared to take action should a problem arise. For this same reason, it’s also a good idea to provide the beneficiary with access to the contract.

Does a beneficiary need to do anything to receive the death benefit?

Technically a beneficiary does not have to do anything to receive your policy’s death benefit, but it’s a good idea to make sure he or she is aware that the policy exists in case there are any delays or complications on the insurer’s side.

The insurer will require proof of death and a copy of the contract in order to disburse the benefit.

Is the life insurance my employer provides enough?

Many employers offer life insurance as part of a benefits package. Usually, the amount is a multiple of your salary, up to a limit (usually one or two times your salary). Whether this is enough protection for your needs depends on your financial situation.

Life insurance is more expensive for those who are older or in poor health, so employer-offered life insurance can be a great way to obtain coverage if you can’t otherwise afford it.

Are my life insurance premiums tax-deductible?

What’s the difference between an agent and a broker?

The difference between an agent and a broker is that an agent usually sells insurance for a single insurer, while a broker sells insurance for any number of insurers.

In some cases, an agent may actually be employed by the insurance company, although there are also agents who are self-employed.

If you’re looking for details about a specific insurer’s products, an agent may be the best person to talk to. However, if you’re trying to comparison shop across multiple insurers, you may want to contact a broker.

Agents and brokers always provide their services for free and earn commissions off of the policies they sell.

What happens to the money I pay into a policy if I outlive the coverage term?

What happens if I can’t pay my policy premiums?

Mortgage Protection FAQ

Whos owns the insurance?

Owned by you. You can control what happens to your life insurance coverage.

Who determines who will get the benefits?

The lender receiving the proceeds, generally applies it to pay off the mortgage.

You decide who will be named beneficiary and receive the proceeds.

Can my coverage be canceled by someone other than myself? Will I get the benefits?

Your policy may be canceled by the lender or issuing company. Often, coverage ends with the expiry/cancellation of the mortgage.

No. Although your coverage offers mortgage protection it is not tied to a specific mortgage or need. When your mortgage is finished your coverage may remain in force, except in the event of non-payment of your life insurance premiums.

Can I continue the coverage if I change companies or move?

Your insurance may end when the mortgage is repaid, assumed, canceled, the house is sold or the group policy terminates.

Yes. Coverage is portable and you can use it to cover another mortgage, if desired.

Is the benefit amount level?

Benefit typically declines in line with the outstanding mortgage balance, if it is decreasing term insurance.

Yes. Amount of benefit can remain level even though the mortgage balance reduces.

Can I apply for more coverage than the mortgage amount?

Amount of benefit may only be for the amount of the mortgage, and there are limited options if your health changes.

Yes. Coverage can be higher than the amount of the mortgage to cover other needs.

Can the plan be designed to build cash values?

These plans are typically group decreasing term only.

Yes. Depending on the life insurance coverage you choose you may be able to take advantage of tax-deferred cash accumulation options.

Can my plan be customized to meet my individual needs?

Yes. Other benefits and features can often be added through optional riders.